In this lecture we discuss under which assumptions the OLS (Ordinary Least Squares) estimator has desirable statistical properties such as consistency and asymptotic normality.

![]()

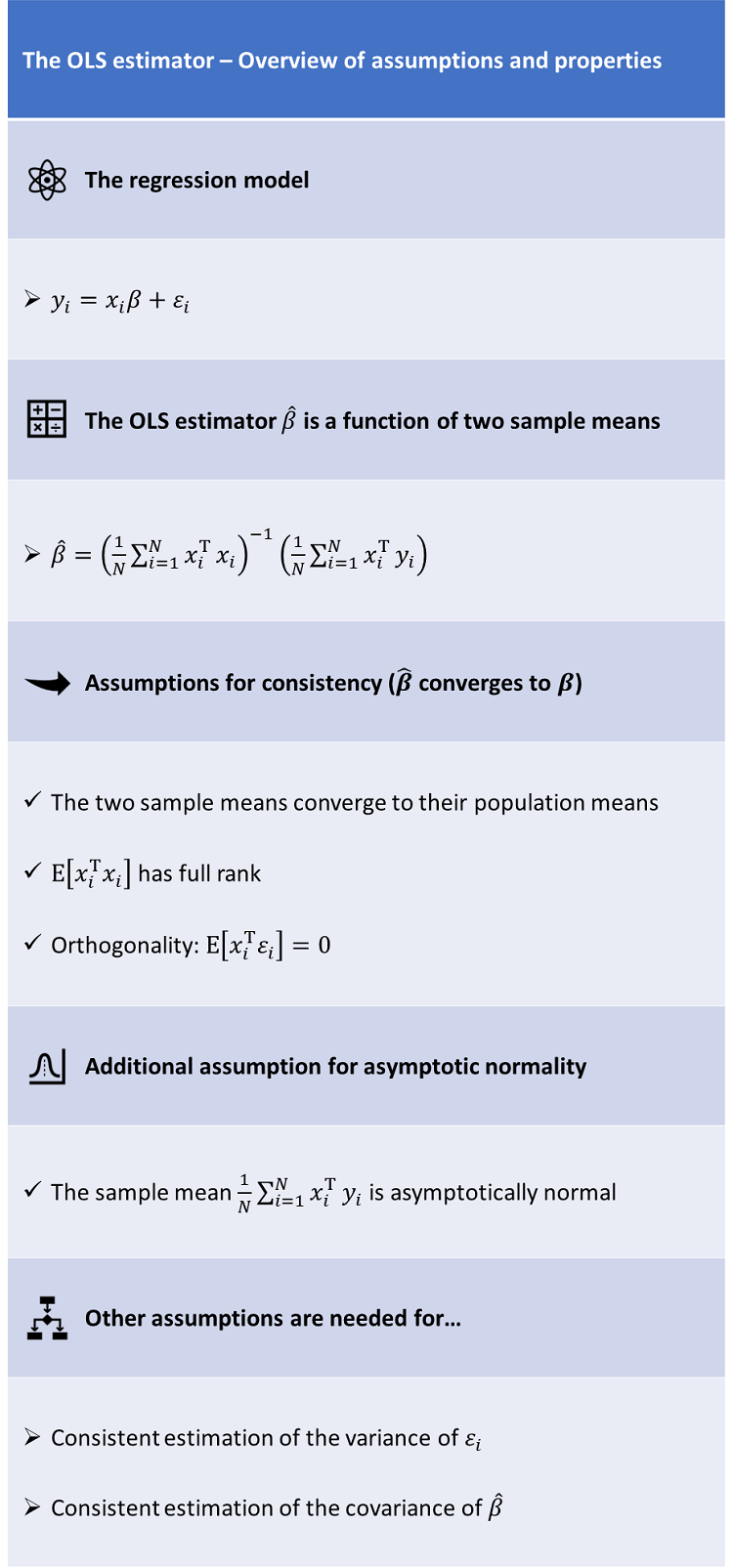

Consider the linear

regression

model![]() where:

where:

the outputs are denoted by

![]() ;

;

the associated

![]() vectors of inputs are denoted by

vectors of inputs are denoted by

![]() ;

;

the

![]() vector of regression coefficients is denoted by

vector of regression coefficients is denoted by

![]() ;

;

![]() are unobservable error terms.

are unobservable error terms.

We assume to observe a sample of

![]() realizations, so that the vector of all outputs

realizations, so that the vector of all outputs

![[eq2]](data:image/gif;base64,R0lGODlhAQABAIAAANvf7wAAACH5BAEAAAAALAAAAAABAAEAAAICRAEAOw==) is

an

is

an

![]() vector, the design

matrixis

an

vector, the design

matrixis

an

![]() matrix, and the vector of error

termsis

an

matrix, and the vector of error

termsis

an

![]() vector.

vector.

The OLS estimator

![]() is the vector of regression coefficients that minimizes the sum of squared

residuals:

is the vector of regression coefficients that minimizes the sum of squared

residuals:

As proved in the lecture on

Linear

regression, if the design matrix

![]() has full rank, then the OLS estimator is computed as

follows:

has full rank, then the OLS estimator is computed as

follows:![]()

The OLS estimator can be written as

where

is

the sample mean of the

![]() matrix

matrix

![]() and

is

the sample mean of the

and

is

the sample mean of the

![]() matrix

matrix

![]() .

.

In this section we are going to propose a set of conditions that are

sufficient for the consistency

of the OLS estimator, that is, for the convergence in probability of

![]() to the true value

to the true value

![]() .

.

The first assumption we make is that the sample means in the OLS formula converge to their population counterparts, which is formalized as follows.

Assumption 1 (convergence): both the sequence

![]() and the sequence

and the sequence

![]() satisfy sets of conditions that are sufficient for the

convergence in probability of their sample means

to the population means

satisfy sets of conditions that are sufficient for the

convergence in probability of their sample means

to the population means

![]() and

and

![]() ,

which do not depend on

,

which do not depend on

![]() .

.

For example, the sequences

![]() and

and

![]() could be assumed to satisfy the conditions of

Chebyshev's Weak Law of Large Numbers for

correlated sequences, which are quite mild (basically, it is only required

that the sequences are

covariance stationary and

that their auto-covariances are zero on average).

could be assumed to satisfy the conditions of

Chebyshev's Weak Law of Large Numbers for

correlated sequences, which are quite mild (basically, it is only required

that the sequences are

covariance stationary and

that their auto-covariances are zero on average).

The second assumption we make is a rank assumption (sometimes also called identification assumption).

Assumption 2 (rank): the square matrix

![]() has full rank (as a

consequence, it is invertible).

has full rank (as a

consequence, it is invertible).

The third assumption we make is that the regressors

![]() are orthogonal to the error terms

are orthogonal to the error terms

![]() .

.

Assumption 3 (orthogonality): For each

![]() ,

,

![]() and

and

![]() are orthogonal, that

is,

are orthogonal, that

is,![]()

It is then straightforward to prove the following proposition.

Proposition

If Assumptions 1, 2 and 3 are satisfied, then the OLS estimator

![]() is a consistent estimator of

is a consistent estimator of

![]() .

.

Let us make explicit the dependence of the

estimator on the sample size and denote by

![]() the OLS estimator obtained when the sample size is equal to

the OLS estimator obtained when the sample size is equal to

![]() By Assumption 1 and by the

Continuous Mapping

theorem, we have that the probability limit of

By Assumption 1 and by the

Continuous Mapping

theorem, we have that the probability limit of

![]() is

is

![[eq20]](/images/OLS-estimator-properties__47.png) Now,

if we pre-multiply the regression

equation

Now,

if we pre-multiply the regression

equation![]() by

by

![]() and we take expected values, we

get

and we take expected values, we

get![]() But

by Assumption 3, it

becomes

But

by Assumption 3, it

becomes![]() or

or![]() which

implies

that

which

implies

that

We now introduce a new assumption, and we use it to prove the asymptotic normality of the OLS estimator.

The assumption is as follows.

Assumption 4 (Central Limit Theorem): the sequence

![]() satisfies a set of conditions that are sufficient to guarantee that a Central

Limit Theorem applies to its sample

mean

satisfies a set of conditions that are sufficient to guarantee that a Central

Limit Theorem applies to its sample

mean

For a review of some of the conditions that can be imposed on a sequence to guarantee that a Central Limit Theorem applies to its sample mean, you can go to the lecture on the Central Limit Theorem.

In any case, remember that if a Central Limit Theorem applies to

![]() ,

then, as

,

then, as

![]() tends to

infinity, converges

in distribution to a multivariate normal

distribution with mean equal to

tends to

infinity, converges

in distribution to a multivariate normal

distribution with mean equal to

![]() and covariance matrix equal

to

and covariance matrix equal

to

With Assumption 4 in place, we are now able to prove the asymptotic normality of the OLS estimator.

Proposition

If Assumptions 1, 2, 3 and 4 are satisfied, then the OLS estimator

![]() is asymptotically multivariate normal with mean equal to

is asymptotically multivariate normal with mean equal to

![]() and asymptotic covariance matrix equal

to

and asymptotic covariance matrix equal

to![]() that

is,

that

is,![]() where

where

![]() has been defined above.

has been defined above.

As in the proof of consistency, the

dependence of the estimator on the sample size is made explicit, so that the

OLS estimator is denoted by

![]() .

First of all, we have

.

First of all, we have

![[eq34]](/images/OLS-estimator-properties__67.png) where,

in the last step, we have used the fact that, by Assumption 3,

where,

in the last step, we have used the fact that, by Assumption 3,

![]() .

Note that, by Assumption 1 and the Continuous Mapping theorem, we

haveFurthermore,

by Assumption 4, we have

thatconverges

in distribution to a multivariate normal random vector having mean equal to

.

Note that, by Assumption 1 and the Continuous Mapping theorem, we

haveFurthermore,

by Assumption 4, we have

thatconverges

in distribution to a multivariate normal random vector having mean equal to

![]() and covariance matrix equal to

and covariance matrix equal to

![]() .

Thus, by Slutski's theorem, we have

that

.

Thus, by Slutski's theorem, we have

that![[eq38]](/images/OLS-estimator-properties__73.png) converges

in distribution to a multivariate normal vector with mean equal to

converges

in distribution to a multivariate normal vector with mean equal to

![]() and covariance matrix equal to

and covariance matrix equal to

![]()

We now discuss the consistent estimation of the variance of the error terms.

Here is an additional assumption.

Assumption 5: the sequence

![]() satisfies a set of conditions that are sufficient for the convergence in

probability of its sample

meanto

the population mean

satisfies a set of conditions that are sufficient for the convergence in

probability of its sample

meanto

the population mean

![]() which

does not depend on

which

does not depend on

![]() .

.

If this assumption is satisfied, then the variance of the error terms

![]() can be estimated by the sample variance of the

residualswhere

can be estimated by the sample variance of the

residualswhere

![]()

Proposition

Under Assumptions 1, 2, 3, and 5, it can be proved that

is a consistent estimator of

![]() .

.

Let us make explicit the dependence of the

estimators on the sample size and denote by

![]() and

and

![]() the estimators obtained when the sample size is equal to

the estimators obtained when the sample size is equal to

![]() By Assumption 1 and by the

Continuous Mapping

theorem, we have that the probability limit of

By Assumption 1 and by the

Continuous Mapping

theorem, we have that the probability limit of

![]() is

is

![[eq49]](/images/OLS-estimator-properties__89.png) where:

in steps

where:

in steps

![]() and

and

![]() we have used the Continuous Mapping Theorem; in step

we have used the Continuous Mapping Theorem; in step

![]() we have used Assumption 5; in step

we have used Assumption 5; in step

![]() we have used the fact that

because

we have used the fact that

because

![]() is a consistent estimator of

is a consistent estimator of

![]() ,

as proved above.

,

as proved above.

We have proved that the asymptotic covariance matrix of the OLS estimator

is![]() where

the long-run covariance matrix

where

the long-run covariance matrix

![]() is defined

by

is defined

by

Usually, the matrix

![]() needs to be estimated because it depends on quantities

(

needs to be estimated because it depends on quantities

(![]() and

and

![]() )

that are not known.

)

that are not known.

The next proposition characterizes consistent estimators of

![]() .

.

Proposition

If Assumptions 1, 2, 3, 4 and 5 are satisfied, and a consistent estimator

![]() of the long-run covariance matrix

of the long-run covariance matrix

![]() is available, then the asymptotic variance of the OLS estimator is

consistently estimated

by

is available, then the asymptotic variance of the OLS estimator is

consistently estimated

by

This is proved as

followswhere:

in step

![]() we have used the Continuous Mapping theorem; in step

we have used the Continuous Mapping theorem; in step

![]() we have used the hypothesis that

we have used the hypothesis that

![]() is a consistent estimator of the long-run covariance matrix

is a consistent estimator of the long-run covariance matrix

![]() and the fact that, by Assumption 1, the sample mean of the matrix

and the fact that, by Assumption 1, the sample mean of the matrix

![]() is a consistent estimator of

is a consistent estimator of

![]() ,

that

is

,

that

is![]()

Thus, in order to derive a consistent estimator of the covariance matrix of

the OLS estimator, we need to find a consistent estimator of the long-run

covariance matrix

![]() .

How to do this is discussed in the next section.

.

How to do this is discussed in the next section.

The estimation of

![]() requires some assumptions on the covariances between the terms of the sequence

requires some assumptions on the covariances between the terms of the sequence

![]() .

.

In order to find a simpler expression for

![]() ,

we make the following assumption.

,

we make the following assumption.

Assumption 6: the sequence

![]() is serially

uncorrelated, that

is,

is serially

uncorrelated, that

is,![]() and

weakly stationary, that is,

and

weakly stationary, that is,

![]() does

not depend on

does

not depend on

![]() .

.

Remember that in Assumption 3 (orthogonality) we also ask

that![]()

We now derive simpler expressions for

![]() .

.

Proposition

Under Assumptions 3 (orthogonality), the long-run covariance matrix

![]() satisfies

satisfies

This is proved as

follows:![[eq67]](/images/OLS-estimator-properties__128.png)

Proposition

Under Assumptions 3 (orthogonality) and 6 (no serial correlation), the

long-run covariance matrix

![]() satisfies

satisfies![]()

The proof is as

follows:![[eq69]](/images/OLS-estimator-properties__131.png)

Thanks to assumption 6, we can also derive an estimator of

![]() .

.

Proposition

Suppose that Assumptions 1, 2, 3, 4 and 6 are satisfied, and that

![]() is consistently estimated by the sample

meanThen,

the long-run covariance matrix

is consistently estimated by the sample

meanThen,

the long-run covariance matrix

![]() is consistently estimated

by

is consistently estimated

by

We

have![[eq73]](/images/OLS-estimator-properties__137.png) where

in the last step we have applied the Continuous Mapping theorem separately to

each entry of the matrices in square brackets, together with the fact that

To

see how this is done, consider, for example, the

matrixThen,

the entry at the intersection of its

where

in the last step we have applied the Continuous Mapping theorem separately to

each entry of the matrices in square brackets, together with the fact that

To

see how this is done, consider, for example, the

matrixThen,

the entry at the intersection of its

![]() -th

row and

-th

row and

![]() -th

column

isand

-th

column

isand

When the assumptions of the previous proposition hold, the asymptotic

covariance matrix of the OLS estimator

is

As a consequence, the covariance of the OLS estimator can be approximated

bywhich

is known as

heteroskedasticity-robust

estimator.

A further assumption is often made, which allows us to further simplify the expression for the long-run covariance matrix.

Assumption 7: the error terms are

conditionally

homoskedastic:![]()

This assumption has the following implication.

Proposition

Suppose that Assumptions 1, 2, 3, 4, 5, 6 and 7 are satisfied. Then, the

long-run covariance matrix

![]() is consistently estimated

by

is consistently estimated

by

First of all, we have

that![[eq82]](/images/OLS-estimator-properties__149.png) But

we know that, by Assumption 1,

But

we know that, by Assumption 1,

![]() is consistently estimated

byand

by Assumptions 1, 2, 3 and 5,

is consistently estimated

byand

by Assumptions 1, 2, 3 and 5,

![]() is consistently estimated

byTherefore,

by the Continuous Mapping theorem, the long-run covariance matrix

is consistently estimated

byTherefore,

by the Continuous Mapping theorem, the long-run covariance matrix

![]() is consistently estimated by

is consistently estimated by

When the assumptions of the previous proposition hold, the asymptotic

covariance matrix of the OLS estimator

is

As a consequence, the covariance of the OLS estimator can be approximated

bywhich

is the same estimator derived in the

normal

linear regression model.

The assumptions above can be made even weaker (for example, by relaxing the

hypothesis that

![]() is uncorrelated with

is uncorrelated with

![]() ),

at the cost of facing more difficulties in estimating the long-run covariance

matrix.

),

at the cost of facing more difficulties in estimating the long-run covariance

matrix.

For a review of the methods that can be used to estimate

![]() ,

see, for example, Den and Levin (1996).

,

see, for example, Den and Levin (1996).

The lecture entitled Linear regression - Hypothesis testing discusses how to carry out hypothesis tests on the coefficients of a linear regression model in the cases discussed above, that is, when the OLS estimator is asymptotically normal and a consistent estimator of the asymptotic covariance matrix is available.

Haan, Wouter J. Den, and Andrew T. Levin (1996). "Inferences from parametric and non-parametric covariance matrix estimation procedures." Technical Working Paper Series, NBER.

Please cite as:

Taboga, Marco (2021). "Properties of the OLS estimator", Lectures on probability theory and mathematical statistics. Kindle Direct Publishing. Online appendix. https://www.statlect.com/fundamentals-of-statistics/OLS-estimator-properties.

Most of the learning materials found on this website are now available in a traditional textbook format.