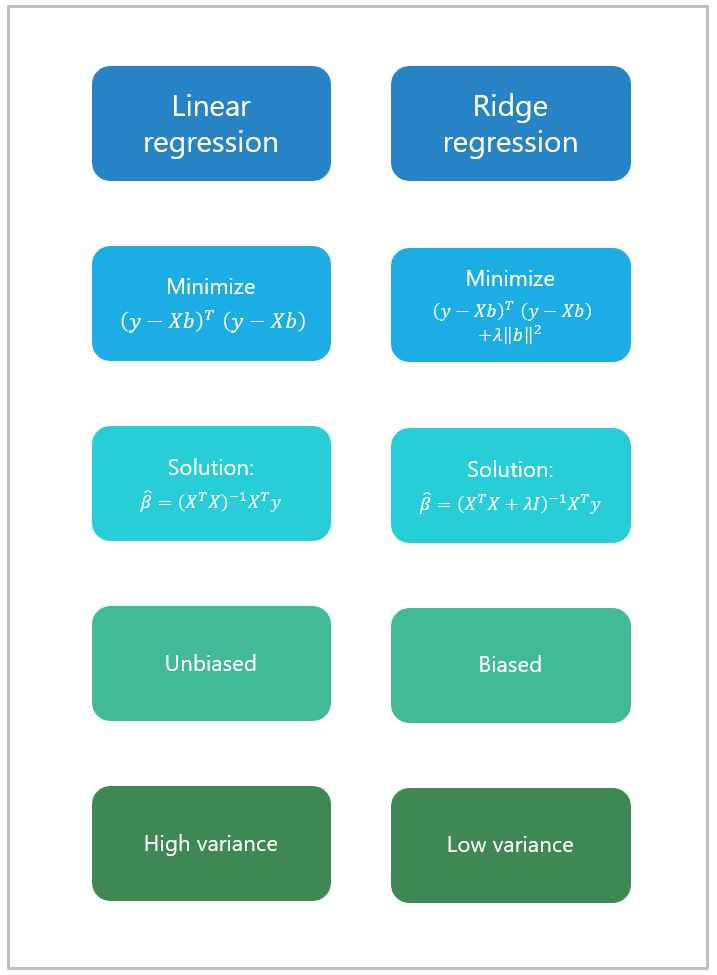

Ridge regression is a term used to refer to a linear regression model whose coefficients are estimated not by ordinary least squares (OLS), but by an estimator, called ridge estimator, that, albeit biased, has lower variance than the OLS estimator.

In certain cases, the mean squared error of the ridge estimator (which is the sum of its variance and the square of its bias) is smaller than that of the OLS estimator.

![]()

Ridge estimation is carried out on the linear regression

model![]() where:

where:

![]() is the

is the

![]() vector of observations of

the dependent variable;

vector of observations of

the dependent variable;

![]() is the

is the

![]() matrix of regressors (there are

matrix of regressors (there are

![]() regressors);

regressors);

![]() is the

is the

![]() vector of regression coefficients;

vector of regression coefficients;

![]() is the

is the

![]() vector of errors.

vector of errors.

Remember that the OLS estimator

![]() solves the minimization

problem

solves the minimization

problem![[eq2]](data:image/gif;base64,R0lGODlhAQABAIAAANvf7wAAACH5BAEAAAAALAAAAAABAAEAAAICRAEAOw==) where

where

![]() is the

is the

![]() -th

row of

-th

row of

![]() and

and

![]() and

and

![]() are

are

![]() column vectors.

column vectors.

When

![]() has full rank, the solution to

the OLS problem

is

has full rank, the solution to

the OLS problem

is![]()

The ridge estimator

![]() solves the slightly modified minimization

problemwhere

solves the slightly modified minimization

problemwhere

![]() is a positive constant.

is a positive constant.

Thus, in ridge estimation we add a penalty to the least squares criterion: we

minimize the sum of squared

residualsplus

the squared norm of of the vector of

coefficients

The ridge problem penalizes large regression coefficients, and the larger the

parameter

![]() is, the larger the penalty.

is, the larger the penalty.

We will discuss below how to choose the penalty parameter

![]() .

.

The solution to the minimization problem

is![]() where

where

![]() is the

is the

![]() identity matrix.

identity matrix.

The objective function to minimize can be

written in matrix form as

follows:The

first order condition for a minimum is that the gradient of

![]() with respect to

with respect to

![]() should be equal to

zero:

should be equal to

zero:![]() that

is,

that

is,![]() or

or![]() The

matrix

The

matrix![]() is

positive definite for

any

is

positive definite for

any

![]() because, for any

because, for any

![]() vector

vector

![]() ,

we

havewhere

the last inequality follows from the fact that even if

,

we

havewhere

the last inequality follows from the fact that even if

![]() is equal to

is equal to

![]() for every

for every

![]() ,

,

![]() is strictly positive for at least one

is strictly positive for at least one

![]() .

Therefore, the matrix has full

rank and it is invertible.

As a consequence, the first order condition is satisfied

by

.

Therefore, the matrix has full

rank and it is invertible.

As a consequence, the first order condition is satisfied

by![]() We

now need to check that this is indeed a global minimum. Note that the Hessian

matrix, that is, the matrix of second derivatives of

We

now need to check that this is indeed a global minimum. Note that the Hessian

matrix, that is, the matrix of second derivatives of

![]() ,

is

,

is![]() Thus,

the Hessian is positive definite (it is a positive multiple of a matrix that

we have just proved to be positive definite). Hence,

Thus,

the Hessian is positive definite (it is a positive multiple of a matrix that

we have just proved to be positive definite). Hence,

![]() is strictly convex in

is strictly convex in

![]() ,

which implies that

,

which implies that

![]() is a global minimum.

is a global minimum.

If you read the proof above, you will notice that, unlike in OLS estimation,

we do not need to assume that the design matrix

![]() is full-rank. Therefore, the ridge estimator exists also when

is full-rank. Therefore, the ridge estimator exists also when

![]() does not have full rank.

does not have full rank.

In this section we derive the bias and variance of the ridge estimator under

the commonly made assumption (e.g., in the

normal

linear regression model) that,

conditional

on

![]() ,

the errors of the regression have zero mean and constant variance

,

the errors of the regression have zero mean and constant variance

![]() and are

uncorrelated:where

and are

uncorrelated:where

![]() is a positive constant and

is a positive constant and

![]() is the

is the

![]() identity matrix.

identity matrix.

The conditional expected value of the ridge estimator

![]() is

is![]() which

is different from

which

is different from

![]() unless

unless

![]() (the OLS case).

(the OLS case).

The bias of the estimator

is![]()

We can write the ridge estimator

asTherefore,

![[eq22]](/images/ridge-regression__67.png) The

ridge estimator is unbiased, that

is,

The

ridge estimator is unbiased, that

is,![]() if

and only

if

if

and only

if![]() But

this is possible if only if

But

this is possible if only if

![]() ,

that is, if the ridge estimator coincides with the OLS estimator. where

,

that is, if the ridge estimator coincides with the OLS estimator. where

![]() is the

is the

![]() identity matrix. The bias

is

identity matrix. The bias

is

The covariance

matrix of the ridge estimator

is![]()

Remember that the OLS estimator

![]() has conditional

variance

has conditional

variance![]() We

can write the ridge estimator as a function of the OLS

estimator:Therefore,

We

can write the ridge estimator as a function of the OLS

estimator:Therefore,![[eq29]](/images/ridge-regression__78.png)

Importantly, the variance of the ridge estimator is always smaller than the variance of the OLS estimator.

More precisely, the difference between the covariance matrix of the OLS

estimator and that of the ridge estimator

![]() is

positive definite (remember from the lecture on the

Gauss-Markov

theorem that the covariance matrices of two estimators are compared by

checking whether their difference is positive definite).

is

positive definite (remember from the lecture on the

Gauss-Markov

theorem that the covariance matrices of two estimators are compared by

checking whether their difference is positive definite).

In order to make a comparison, the OLS

estimator must exist. As a consequence,

![]() must be full-rank. With this assumption in place, the conditional variance of

the OLS estimator

is

must be full-rank. With this assumption in place, the conditional variance of

the OLS estimator

is![]() Now,

define the

matrix

Now,

define the

matrix![]() which

is invertible. Then, we can rewrite the covariance matrix of the ridge

estimator as

follows:

which

is invertible. Then, we can rewrite the covariance matrix of the ridge

estimator as

follows:![[eq33]](/images/ridge-regression__83.png) The

difference between the two covariance matrices

is

The

difference between the two covariance matrices

is![[eq34]](/images/ridge-regression__84.png) If

If

![]() ,

the latter matrix is positive definite because for any

,

the latter matrix is positive definite because for any

![]() ,

we

have

,

we

have![]() andbecause

andbecause

![]() and its inverse are positive definite.

and its inverse are positive definite.

The mean squared error (MSE) of the ridge estimator

is equal to the trace of its

covariance matrix plus the squared norm of its bias (the so-called

bias-variance

decomposition):

The OLS estimator has zero bias, so its MSE

is

The difference between the two MSEs

is![[eq39]](/images/ridge-regression__92.png) where

we have used the fact that the sum of the traces of two matrices is equal to

the trace of their sum.

where

we have used the fact that the sum of the traces of two matrices is equal to

the trace of their sum.

We have a difference between two terms

(![]() and

and

![]() ).

We have already proved that the

matrix

).

We have already proved that the

matrix![]() is

positive definite. As a consequence, its trace (term

is

positive definite. As a consequence, its trace (term

![]() )

is strictly positive.

)

is strictly positive.

The square of the bias (term

![]() )

is also strictly positive. Therefore, the difference between

)

is also strictly positive. Therefore, the difference between

![]() and

and

![]() could

in principle be either positive or negative.

could

in principle be either positive or negative.

It is possible to prove (see Theobald 1974 and

Farebrother 1976) that whether the difference is

positive or negative depends on the penalty parameter

![]() ,

and it is always possible to find a value for

,

and it is always possible to find a value for

![]() such that the difference is positive.

such that the difference is positive.

Thus, there always exists a value of the penalty parameter such that the ridge estimator has lower mean squared error than the OLS estimator.

This result is very important from both a practical and a theoretical standpoint. Although, by the Gauss-Markov theorem, the OLS estimator has the lowest variance (and the lowest MSE) among the estimators that are unbiased, there exists a biased estimator (a ridge estimator) whose MSE is lower than that of OLS.

We have just proved that there exists a

![]() such that the ridge estimator is better (in the MSE sense) than the OLS one.

such that the ridge estimator is better (in the MSE sense) than the OLS one.

The question is: how do find the optimal

![]() ?

?

The most common way to find the best

![]() is by so-called leave-one-out cross-validation:

is by so-called leave-one-out cross-validation:

we choose a grid of

![]() possible values

possible values

![]() for the penalty parameter;

for the penalty parameter;

for

![]() ,

we exclude the

,

we exclude the

![]() -th

observation

-th

observation

![]() from the sample and we:

from the sample and we:

use the remaining

![]() observations to compute

observations to compute

![]() ridge estimates of

ridge estimates of

![]() ,

denoted by

,

denoted by

![]() ,

where the subscripts

,

where the subscripts

![]() indicate that the penalty parameter is set equal to

indicate that the penalty parameter is set equal to

![]() (

(![]() )

and the

)

and the

![]() -th

observation has been excluded;

-th

observation has been excluded;

compute

![]() out-of-sample predictions of the excluded

observation

out-of-sample predictions of the excluded

observation![]() for

for

![]() .

.

we compute the MSE of the

predictionsfor

![]() .

.

we choose as the optimal penalty parameter

![]() the one that minimizes the MSE of the

predictions:

the one that minimizes the MSE of the

predictions:![]()

In other words, we set

![]() equal to the value that generates the lowest MSE in the leave-one-out

cross-validation exercise.

equal to the value that generates the lowest MSE in the leave-one-out

cross-validation exercise.

Our lecture on the

choice of

regularization parameters provides an example (with Python code) of how to

choose

![]() by using a cross-validation method called hold-out cross-validation.

by using a cross-validation method called hold-out cross-validation.

A nice property of the OLS estimator is that it is scale invariant: if we

post-multiply the design matrix by an invertible matrix

![]() ,

then the OLS estimate we obtain is equal to the previous estimate multiplied

by

,

then the OLS estimate we obtain is equal to the previous estimate multiplied

by

![]() .

.

For example, if we multiply a regressor by 2, then the OLS estimate of the coefficient of that regressor is divided by 2.

In more formal terms, consider the OLS estimate

![]() and

the rescaled design matrix

and

the rescaled design matrix

![]()

The OLS estimate associated to the new design matrix

is

Thus, no matter how we rescale the regressors, we always obtain the same result.

This is a nice property of the OLS estimator that is unfortunately not possessed by the ridge estimator.

Consider the estimate

![]()

Then, the ridge estimate associated to the rescaled matrix

![]() iswhich

is equal to

iswhich

is equal to

![]() only

if

only

if![]() that

is, only

if

that

is, only

if![]()

In other words, the ridge estimator is scale-invariant only in the special

case in which the scale matrix

![]() is orthonormal.

is orthonormal.

The general absence of scale-invariance implies that any choice we make about the scaling of variables (e.g., expressing a regressor in centimeters vs meters or thousands vs millions of dollars) affects the coefficient estimates.

Since this is highly undesirable, what we usually do is to standardize all the variables in our regression, that is, we subtract from each variable its mean and we divide it by its standard deviation. By doing so, the coefficient estimates are not affected by arbitrary choices of the scaling of variables.

Farebrother, R. W. (1976) " Further results on the mean square error of ridge regression", Journal of the Royal Statistical Society, Series B (Methodological), 38, 248-250.

Theobald, C. M. (1974) " Generalizations of mean square error applied to ridge regression", Journal of the Royal Statistical Society, Series B (Methodological), 36, 103-106.

Please cite as:

Taboga, Marco (2021). "Ridge regression", Lectures on probability theory and mathematical statistics. Kindle Direct Publishing. Online appendix. https://www.statlect.com/fundamentals-of-statistics/ridge-regression.

Most of the learning materials found on this website are now available in a traditional textbook format.