Importance sampling is a variance reduction technique. We use it to reduce the variance of the approximation error that we make when we approximate an expected value with Monte Carlo integration.

In this lecture, we explain how importance sampling works and then we show with an example how effective it can be.

![]()

Importance sampling is based on a simple method used to compute expected values in many different but equivalent ways.

The next proposition shows how the technique works for discrete random vectors.

Proposition

Let

![]() be a

be a

![]() discrete random vector with support

discrete random vector with support

![]() and joint probability

mass function

and joint probability

mass function

![]() .

Let

.

Let

![]() be a function

be a function

![]() .

Let

.

Let

![]() be another

be another

![]() discrete random vector

discrete random vector

![]() with joint probability mass function

with joint probability mass function

![]() and such that

and such that

![]() whenever

whenever

![]() .

Then,

.

Then,

![[eq6]](/images/importance-sampling__13.png)

This is obtained as

follows:![[eq7]](/images/importance-sampling__14.png)

An almost identical proposition holds for continuous random vectors.

Proposition

Let

![]() be a continuous

be a continuous

![]() random vector with support

random vector with support

![]() and joint probability

density function

and joint probability

density function

![]() .

Let

.

Let

![]() be a function

be a function

![]() .

Let

.

Let

![]() be another continuous random vector

be another continuous random vector

![]() with joint probability density function

with joint probability density function

![]() and such that

and such that

![]() whenever

whenever

![]() .

Then,

.

Then,

![[eq13]](/images/importance-sampling__26.png)

This is obtained as

follows:![[eq14]](/images/importance-sampling__27.png) where

we have

used

where

we have

used![[eq15]](data:image/gif;base64,R0lGODlhAQABAIAAANvf7wAAACH5BAEAAAAALAAAAAABAAEAAAICRAEAOw==) as

a shorthand for the multiple integral over the coordinates of

as

a shorthand for the multiple integral over the coordinates of

![]() .

.

Suppose that we need to compute the expected

value![]() of

a function of a random vector

of

a function of a random vector

![]() by Monte Carlo integration.

by Monte Carlo integration.

The standard way to proceed is to produce a computer-generated sample of

realizations of

![]() independent random vectors

independent random vectors

![]() ,...,

,...,![]() having the same distribution as

having the same distribution as

![]() .

.

Then, we use the sample mean

to

approximate the expected value.

Thanks to the propositions in the previous section, we can compute an

alternative Monte Carlo approximation of

![]() by extracting

by extracting

![]() independent draws

independent draws

![]() from the distribution of another random vector

from the distribution of another random vector

![]() (in what follows we assume that it is discrete, but everything we say applies

also to continuous vectors).

(in what follows we assume that it is discrete, but everything we say applies

also to continuous vectors).

Then, we use the sample

meanas

an approximation.

This technique is called importance sampling.

The reason why we use importance sampling is that we can often choose

![]() in such a way that the variance of the approximation error is much smaller

than the variance of the standard Monte Carlo approximation.

in such a way that the variance of the approximation error is much smaller

than the variance of the standard Monte Carlo approximation.

In the case of the standard Monte Carlo approximation, the variance of the

approximation error

is![]()

In the case of importance sampling, the variance of the approximation error

is

In the standard case, the approximation

error

is![]() and

its variance

is

and

its variance

is![[eq24]](/images/importance-sampling__46.png) In

the case of importance sampling, we

have

In

the case of importance sampling, we

have![[eq25]](/images/importance-sampling__47.png)

Ideally, we would like to be able to choose

![]() in such a way that

is

a constant, which would imply that the variance of the approximation error is

zero.

in such a way that

is

a constant, which would imply that the variance of the approximation error is

zero.

The next proposition shows when this ideal situation is achievable.

Proposition

If

![]() for any

for any

![]() ,

thenwhen

,

thenwhen

![]() has joint probability mass

function

has joint probability mass

function![[eq29]](/images/importance-sampling__54.png)

The ratio

is

constant if the proportionality

condition![]() holds.

By imposing that

holds.

By imposing that

![]() be a legitimate probability density function, we

getor

be a legitimate probability density function, we

getor

Of course, the denominator

![]() is unknown (otherwise we would not be discussing how to compute a Monte Carlo

approximation for it), so that it is not feasible to achieve the optimal

choice for

is unknown (otherwise we would not be discussing how to compute a Monte Carlo

approximation for it), so that it is not feasible to achieve the optimal

choice for

![]() .

.

However, the formula for the probability mass function (pmf) of the optimal

![]() gives us some indications about the choice of

gives us some indications about the choice of

![]() .

.

In particular, equation (1) tells us that the pmf of

![]() should place more mass where the product between the pmf of

should place more mass where the product between the pmf of

![]() and the value of

and the value of

![]() is larger.

is larger.

This product is a measure of the importance of the possible

values of

![]() .

.

Therefore, the pmf of

![]() should be tilted so as to give more weight to the more important values of

should be tilted so as to give more weight to the more important values of

![]() .

.

Before showing an example, let us summarize the main takeaways from this lecture:

importance sampling is a way of computing a Monte Carlo approximation of

![]() ;

;

we extract

![]() independent draws

independent draws

![]() from a distribution that is different from that of

from a distribution that is different from that of

![]()

we use the weighted sample

meanas

an approximation of

![]() ;

;

this approximation has small variance when the pmf of

![]() puts more mass than the pmf of

puts more mass than the pmf of

![]() on the important points;

on the important points;

the important points are those for which

![]() is larger; they give a "substantial contribution" to the expected value;

is larger; they give a "substantial contribution" to the expected value;

when we average our samples, we take into account the fact that we

over-sampled the important points by weighting them down with the

weights

![]() which

are smaller than

which

are smaller than

![]() when

when

![]() is larger than

is larger than

![]() .

.

Let us now illustrate importance sampling with an example.

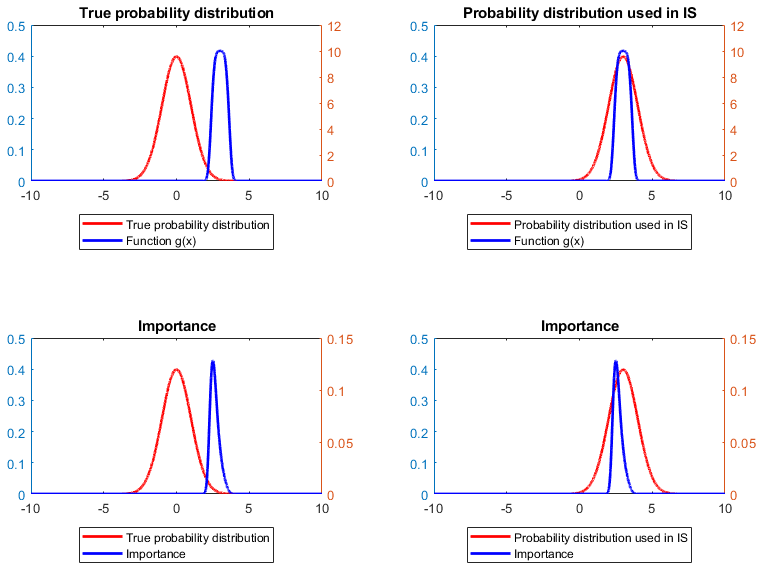

Suppose that

![]() has a standard

normal distribution (i.e., with mean

has a standard

normal distribution (i.e., with mean

![]() and standard deviation

and standard deviation

![]() )

and

)

and

![]()

The function

![]() attains its maximum at the point

attains its maximum at the point

![]() and then rapidly goes to

and then rapidly goes to

![]() for values of

for values of

![]() that are smaller or larger than

that are smaller or larger than

![]() .

.

On the contrary, the probability density function

![]() of a standard normal random variable is almost zero at

of a standard normal random variable is almost zero at

![]() .

.

As a consequence, if we use a standard Monte Carlo approximation:

we extract lots of values of

![]() for which

for which

![]() is almost zero;

is almost zero;

we extract very few values for which

![]() is different from zero.

is different from zero.

This results in a high variance of the approximation error.

In order to shift weight towards

![]() ,

we can sample

,

we can sample

![]() from a normal distribution with mean

from a normal distribution with mean

![]() and standard deviation

and standard deviation

![]() .

.

The following Python code shows how to do so and computes the standard Monte

Carlo (MC) and the importance sampling

(IS) approximations by using samples of

![]() independent draws from the distributions of

independent draws from the distributions of

![]() and

and

![]() .

.

The standard deviations of the two approximations

(std_MC and std_IS) are

estimated by using the sample

variances of

![]() and

and

![]() .

.

If you run this example code, you can see that indeed the importance sampling approximation achieves a significant reduction in the approximation error (from 0.0080 to 0.0012).

# Example of importance sampling in Python

import numpy as np

from scipy.stats import norm

n = 10000 # Number of Monte Carlo samples

np.random.seed(0) # Initialization of random number generator for replicability

# Standard Monte Carlo

x = np.random.randn(n, 1)

g = 10 * np.exp(-5 * (x - 3) ** 4)

MC = np.mean(g)

std_MC = np.sqrt(( 1 / n) * np.var(g))

print('Standard Monte-Carlo estimate of the expected value: ' + str(MC))

print('Standard deviation of plain-vanilla Monte Carlo: ' + str(std_MC))

print(' ')

# Importance sampling

y = 3 + np.random.randn(n, 1);

g = 10 * np.exp(-5 * (y - 3) ** 4);

g_weighted = g * norm.pdf(y, 0, 1) / norm.pdf(y, 3, 1);

IS = np.mean(g_weighted)

std_IS = np.sqrt((1 / n) * np.var(g_weighted))

print('Importance-sampling Monte-Carlo estimate of the expected value: ' + str(IS))

print('Standard deviation of importance-sampling Monte Carlo: ' + str(std_IS))The output is:

Standard Monte-Carlo estimate of the expected value: 0.08579415409780462

Standard deviation of plain-vanilla Monte Carlo: 0.007904811247115087

Importance-sampling Monte-Carlo estimate of the expected value: 0.09096069224808337

Standard deviation of importance-sampling Monte Carlo: 0.0011925073695279826Please cite as:

Taboga, Marco (2021). "Importance sampling", Lectures on probability theory and mathematical statistics. Kindle Direct Publishing. Online appendix. https://www.statlect.com/asymptotic-theory/importance-sampling.

Most of the learning materials found on this website are now available in a traditional textbook format.