The joint distribution function is a function that completely characterizes the probability distribution of a random vector.

![]()

Table of contents

It is also called joint cumulative distribution function (abbreviated as joint cdf).

Let us start with the simple case in which we have two random variables

![]() and

and

![]() .

.

Their joint cdf is defined

as![]() where

where

![]() and

and

![]() are two real numbers.

are two real numbers.

Note that:

![]() indicates a

probability;

indicates a

probability;

the comma inside the parentheses stands for AND.

In other words, the joint cdf

![]() gives the probability that two conditions are simultaneously true:

gives the probability that two conditions are simultaneously true:

the random variable

![]() takes a value less than or equal to

takes a value less than or equal to

![]() ;

;

the random variable

![]() takes a value less than or equal to

takes a value less than or equal to

![]() .

.

Suppose that there are only four possible

cases:![[eq3]](data:image/gif;base64,R0lGODlhAQABAIAAANvf7wAAACH5BAEAAAAALAAAAAABAAEAAAICRAEAOw==)

Further assume that each of these cases has probability equal to 1/4.

Let us compute, as an example, the following value of the joint distribution

function:![]()

The two conditions that need to be simultaneously true

are:

There are two cases in which they are

satisfied:

Therefore, we

have![[eq7]](/images/joint-distribution-function__16.png)

In the previous example we have shown a special case.

In general, the formula for the joint cdf of two discrete random variables

![]() and

and

![]() is:

is:![[eq8]](/images/joint-distribution-function__19.png) where:

where:

![]() is the support of the

vector

is the support of the

vector

![]() ,

that is, the set of all the values of

,

that is, the set of all the values of

![]() that have a strictly positive probability of being observed;

that have a strictly positive probability of being observed;

we sum the probabilities over the

set![]() that

contains all the couples

that

contains all the couples

![]() belonging to the support and such that

belonging to the support and such that

![]() and

and

![]() .

.

The probabilities in the sum are often written using the so-called

joint probability mass

function![]()

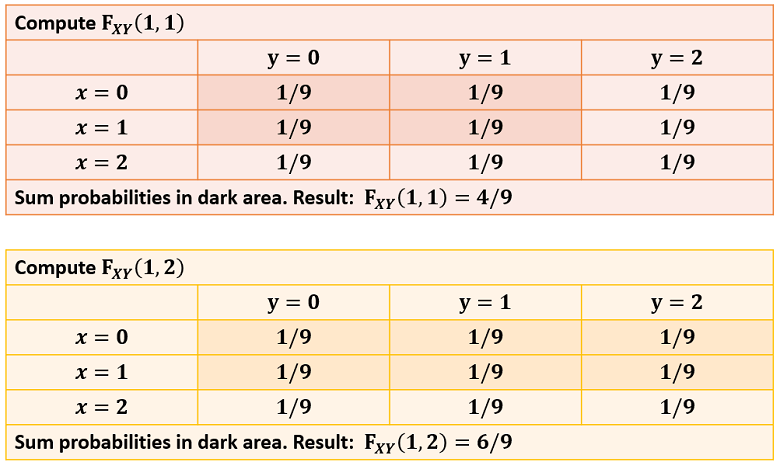

The sum in the formula above can be easily computed with the help of a table.

Here is an example.

In this table, there are nine possible couples

![]() and they all have the same probability (1/9).

and they all have the same probability (1/9).

In order to compute the joint cumulative distribution function, all we need to

do is to shade all the probabilities to the left of

![]() (included) and above

(included) and above

![]() (included).

(included).

Then, the value of

![]() is equal to the sum of the probabilities in the shaded area.

is equal to the sum of the probabilities in the shaded area.

When

![]() and

and

![]() are continuous

random variables, we need to use the

formula

are continuous

random variables, we need to use the

formula![]() where

where

![]() is the joint

probability density function of

is the joint

probability density function of

![]() and

and

![]() .

.

The computation of the double integral can be broken down in two steps:

first compute the inner

integral![]() which,

in general, is a function of

which,

in general, is a function of

![]() and

and

![]() ;

;

then calculate the outer

integral![]()

Let us make an example.

Let the joint pdf

be![[eq17]](/images/joint-distribution-function__42.png)

When

![]() and

and

![]() ,

we have

,

we have

![[eq20]](/images/joint-distribution-function__45.png)

This is only one of the possible cases. We also have the two cases:

![]() or

or

![]() ,

in which

case

,

in which

case![]()

![]() and

and

![]() ,

in which

case

,

in which

case![[eq22]](/images/joint-distribution-function__51.png)

The two marginal

distribution functions of

![]() and

and

![]() are

are

They can be derived from the joint cumulative distribution function as

follows:where

the exact meaning of the notation

is

This can be demonstrated as

follows:![]() because

the condition

because

the condition

![]() is always met and, as a consequence, the condition

is always met and, as a consequence, the condition

![]() is

satisfied whenever

is

satisfied whenever

![]() is true.

is true.

The proof for

![]() is analogous.

is analogous.

In general, we cannot derive the joint cdf from the marginals, unless we know the so-called copula function, which links the two marginals.

However, there is an important exception, discussed in the next section.

When

![]() and

and

![]() are independent, then the joint cdf is equal to the product of the

marginals:

are independent, then the joint cdf is equal to the product of the

marginals:![]()

See the lecture on independent random variables for a proof, a discussion and some examples.

Until now, we have discussed the case of two random variables. However, the joint cdf is defined for any collection of random variables forming a random vector.

Definition

The joint distribution function of a

![]() random vector

random vector

![]() is a function

is a function

![]() such

that:

such

that:![]() where

the entries of

where

the entries of

![]() and

and

![]() are denoted by

are denoted by

![]() and

and

![]() respectively, for

respectively, for

![]() .

.

More details about joint distribution functions can be found in the lecture entitled Random vectors.

Previous entry: Integrable random variable

Next entry: Joint probability density function

Please cite as:

Taboga, Marco (2021). "Joint distribution function", Lectures on probability theory and mathematical statistics. Kindle Direct Publishing. Online appendix. https://www.statlect.com/glossary/joint-distribution-function.

Most of the learning materials found on this website are now available in a traditional textbook format.