Until now we have used the simplest of all cross-validation methods, which consists in testing our predictive models on a subset of the data (the test set) that has not been used for training or selecting the predictive models. This simple cross-validation method is sometimes called the holdout method.

There are more sophisticated cross-validation methods that allow us to obtain better predictive models, together with accurate estimates of an upper bound on the expected loss. In these methods, we perform multiple different partitions of the data into training, validation and test sets, we build a different predictive model for each partition, and finally we average the predictions made by the various models (so-called ensembling).

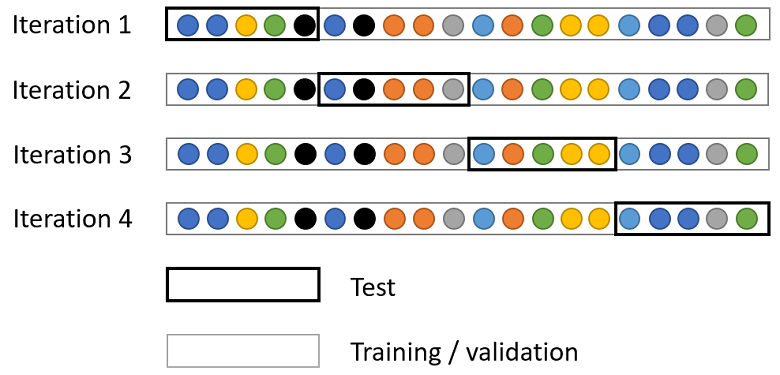

Here we introduce the most popular of these methods, called K-fold cross-validation.

![]()

The data is divided into

![]() subsets, called folds. Each fold contains (approximately) the

same number of observations.

subsets, called folds. Each fold contains (approximately) the

same number of observations.

Then, for

![]() ,

we use the

,

we use the

![]() -th

fold (denoted by

-th

fold (denoted by

![]() )

as the test set and use the remaining

)

as the test set and use the remaining

![]() folds to train a predictive model

folds to train a predictive model

![]() .

.

For each fold, we compute the estimate of the expected loss

![[eq2]](/images/k-fold-cross-validation__7.png) where

where

![]() is a vector of inputs,

is a vector of inputs,

![]() is the loss incurred by using

is the loss incurred by using

![]() as a forecast of the observed output

as a forecast of the observed output

![]() ,

and

,

and

![]() is the number of observations in the

is the number of observations in the

![]() -th

fold.

-th

fold.

Remark: the

![]() folds used to train a predictive model can be divided into training and

validation sets if we need a validation set for model selection.

folds used to train a predictive model can be divided into training and

validation sets if we need a validation set for model selection.

After training the

![]() models

models

![]() ,

we use their ensemble average as our final prediction

,

we use their ensemble average as our final prediction

![[eq7]](/images/k-fold-cross-validation__17.png)

We then compute the average loss

![[eq8]](/images/k-fold-cross-validation__18.png)

As previously discussed, this average is an estimate of an upper bound on the expected loss of the ensemble average (remember that the expected loss of the ensemble average equals the average expected loss of the models in the ensemble minus a correction term that measures the diversity of the models in the ensemble).

K-fold cross validation is straightforward to implement: once we have a

routine for training a predictive model, we just run it

![]() times on the different partitions of the data. The only real disadvantage is

the computational cost.

times on the different partitions of the data. The only real disadvantage is

the computational cost.

As a reward for facing an increased computational cost, we have two main advantages:

our final model (the ensemble average) has been trained on all the data (no data have been "wasted") and it enjoys some benefits from ensembling;

although we no longer have an unbiased

estimate of the expected loss of the final model,

![]() is an estimate of an upper bound to it, which uses all the data in the sample

and should therefore be pretty precise.

is an estimate of an upper bound to it, which uses all the data in the sample

and should therefore be pretty precise.

Let us use K-fold cross-validation to improve on the simpler holdout cross-validation performed when we built a single boosted tree to predict the output variable in an artificially-generated data set.

# Import the packages used to load and manipulate the data

import numpy as np # Numpy is a Matlab-like package for array manipulation and linear algebra

import pandas as pd # Pandas is a data-analysis and table-manipulation tool

import urllib.request # Urlib will be used to download the dataset

# Import the function that performs sample splits from scikit-learn

from sklearn.model_selection import train_test_split

# Load the output variable with pandas (download with urllib if not downloaded previously)

remoteAddress = 'https://www.statlect.com/ml-assets/y_artificial.csv'

localAddress = './y_artificial.csv'

try:

y = pd.read_csv(localAddress, header=None)

except:

urllib.request.urlretrieve(remoteAddress, localAddress)

y = pd.read_csv(localAddress, header=None)

y = y.values # Transform y into a numpy array

# Print some information about the output variable

print('Class and dimension of output variable:')

print(type(y))

print(y.shape)

# Load the input variables with pandas

remoteAddress = 'https://www.statlect.com/ml-assets/x_artificial.csv'

localAddress = './x_artificial.csv'

try:

x = pd.read_csv(localAddress, header=None)

except:

urllib.request.urlretrieve(remoteAddress, localAddress)

x = pd.read_csv(localAddress, header=None)

x = x.values

# Print some information about the input variables

print('Class and dimension of input variables:')

print(type(x))

print(x.shape)The output is:

Class and dimension of output variable:

class 'numpy.ndarray'

(500, 1)

Class and dimension of input variables:

class 'numpy.ndarray'

(500, 300)We create 5 folds using the KFold class provided by the scikit-learn package.

Then, we use LightGBM to make predictions on each fold.

#Import the lightGBM package

import lightgbm as lgb

# Import the functions that performs sample splits from scikit-learn

from sklearn.model_selection import train_test_split, KFold

# Import model-evaluation metrics from scikit-learn

from sklearn.metrics import mean_squared_error, r2_score

# Set number of folds and ensemble variables

n_folds = 5

ensemble = []

mses_single_models = []

mses_constant_predictions = []

r_squareds_single_models = []

# Initialize k_fold splitter

K_fold = KFold(n_splits=n_folds, random_state=0, shuffle=True)

# Iterate over folds

for train_val_index, test_index in K_fold.split(x):

# Get train_val (K-1 folds) and test (1 fold)

x_train_val, x_test = x[train_val_index], x[test_index]

y_train_val, y_test = y[train_val_index], y[test_index]

# Partition the train_val set

x_train, x_val, y_train, y_val

= train_test_split(x_train_val, y_train_val, test_size=0.25, random_state=0)

# Prepare dataset in LightGMB format

y_train = np.squeeze(y_train)

y_val = np.squeeze(y_val)

train_set = lgb.Dataset(x_train, y_train, silent=True)

valid_set = lgb.Dataset(x_val, y_val, silent=True)

# Set algorithm parameters

params = {

'objective': 'regression',

'learning_rate': 0.10,

'metric': 'mse',

'nthread': 8,

'min_data_in_leaf': 10,

'max_depth': 2,

'verbose': -1

}

# Train the model

boosted_tree = lgb.train(

params = params,

train_set = train_set,

valid_sets = valid_set,

num_boost_round = 10000,

early_stopping_rounds = 20,

verbose_eval = False,

)

# Save the model in the ensemble list

ensemble.append(boosted_tree)

# Make predictions on test and compute performance metrics

y_test_pred = boosted_tree.predict(x_test)

mses_single_models.append(mean_squared_error(y_test, y_test_pred))

mses_constant_predictions.append(mean_squared_error(y_test, 0*y_test + np.mean(y_train)))

r_squareds_single_models.append(r2_score(y_test, y_test_pred))

# Print performance metrics on test sample

print('Test MSEs of models in the ensemble:')

print(mses_single_models)

print('Test MSEs of constant predictions equal to sample mean on training set:')

print(mses_constant_predictions)

print('Average test MSE of models in the ensemble:')

print(np.mean(mses_single_models))

print('')

print('Test R squareds of models in the ensemble:')

print(r_squareds_single_models)

print('Average test R squared of models in the ensemble:')

print(np.mean(r_squareds_single_models))

The output is:

Test MSEs of models in the ensemble:

[74.57708434382333, 37.439965145009516, 16.801894170417487, 54.55429632149937, 30.007456926513534]

Test MSEs of constant predictions equal to sample mean on training set:

[293.2026939915153, 167.6726253022108, 104.80130552664033, 213.67954000052373, 131.20844137862687]

Average test MSE of models in the ensemble:

42.67613938145264

Test R squareds of models in the ensemble:

[0.7414010556669601, 0.7762513029977958, 0.8356878267813256, 0.7416211645498416, 0.7712684886703587]

Average test R squared of models in the ensemble:

0.7732459677332564There is significant variation in test mean squared errors (MSEs) across the folds, although it is mostly due to differences in variance (test MSEs of constant predictions). The R squareds are more homogeneous, that is, the proportion of variance explained by the predictions is more stable across folds.

Anyway, the variability in test MSEs reveals that it was probably a good idea to run a K-fold cross-validation.

At this stage, it is not possible to say anything more precise about the benefits from using K-fold cross-validation instead of the simple holdout method (although there are good theoretical guarantees about them). The benefits are likely to become apparent when we put the model in production, which we simulate below.

We now see how our predictive model performs in production, on new data that becomes available after we have completed the training.

# Load the input and output variables with pandas

y_production = pd.read_csv('./assets/y_artificial_production.csv', header=None)

y_production = y_production.values

y_production = np.squeeze(y_production)

x_production = pd.read_csv('./assets/x_artificial_production.csv', header=None)

x_production = x_production.values

# Initialize ensemble variables on production dataset

y_production_pred_ensemble = 0

production_mses_single_models = []

production_r_squareds_single_models = []

# Make predictions with all models in the ensemble and compute ensemble average

for model in ensemble:

y_production_pred = model.predict(x_production)

production_mses_single_models.append(mean_squared_error(y_production, y_production_pred))

production_r_squareds_single_models.append(r2_score(y_production, y_production_pred))

y_production_pred_ensemble += y_production_pred/n_folds

# Print MSEs

print('Production MSEs of models in the ensemble:')

print(production_mses_single_models)

print('Average production MSE of models in the ensemble:')

print(np.mean(production_mses_single_models))

print('Production MSE of ensemble average:')

print(mean_squared_error(y_production, y_production_pred_ensemble))

print('')

# Print R squareds

print('Production R squareds of models in the ensemble:')

print(production_r_squareds_single_models)

print('Average production R squared of models in the ensemble:')

print(np.mean(production_r_squareds_single_models))

print('Production R squared of ensemble average:')

print(r2_score(y_production, y_production_pred_ensemble))The output is:

Production MSEs of models in the ensemble:

[39.64176656361246, 32.90628594145072, 37.6388748646386, 44.169307277678485, 43.86534683792454]

Average production MSE of models in the ensemble:

39.64431629706096

Production MSE of ensemble average:

33.64136466519085

Production R squareds of models in the ensemble:

[0.7639469310457051, 0.8040543987387033, 0.7758734614027009, 0.736986985185174, 0.73879696493291]

Average production R squared of models in the ensemble:

0.7639317482610387

Production R squared of ensemble average:

0.7996772580685613This is an excellent result! The performance of the ensemble average is significantly better than the average performance of the models in the ensemble.

Please cite as:

Taboga, Marco (2021). "K-fold cross-validation", Lectures on machine learning. https://www.statlect.com/machine-learning/k-fold-cross-validation.

Most of the learning materials found on this website are now available in a traditional textbook format.