Linear correlation is a measure of dependence between two random variables.

It has the following characteristics:

it ranges between -1 and 1;

it is proportional to covariance;

its interpretation is very similar to that of covariance (see here).

![]()

Let

![]() and

and

![]() be two random variables.

be two random variables.

The linear correlation coefficient (or Pearson's correlation

coefficient) between

![]() and

and

![]() is

is

![[eq1]](data:image/gif;base64,R0lGODlhAQABAIAAANvf7wAAACH5BAEAAAAALAAAAAABAAEAAAICRAEAOw==) where:

where:

![]() is the covariance between

is the covariance between

![]() and

and

![]() ;

;

![]() and

and

![]() are the standard deviations of

are the standard deviations of

![]() and

and

![]() .

.

The linear correlation coefficient is well-defined only as long as

![]() ,

,

![]() and

and

![]() exist and are well-defined.

exist and are well-defined.

It is often denoted by

![]() .

.

In principle, the ratio is well-defined only if

![]() and

and

![]() are strictly greater than zero.

are strictly greater than zero.

However, it is often assumed that

![]() when one of the two standard deviations is zero.

when one of the two standard deviations is zero.

This is equivalent to assuming that

![]() because

because

![]() when one of the two standard deviations is zero.

when one of the two standard deviations is zero.

The interpretation is similar to the interpretation of covariance: the

correlation between

![]() and

and

![]() provides a measure of how similar their deviations from the respective means

are (see the lecture on Covariance for a detailed

explanation).

provides a measure of how similar their deviations from the respective means

are (see the lecture on Covariance for a detailed

explanation).

Linear correlation ranges between

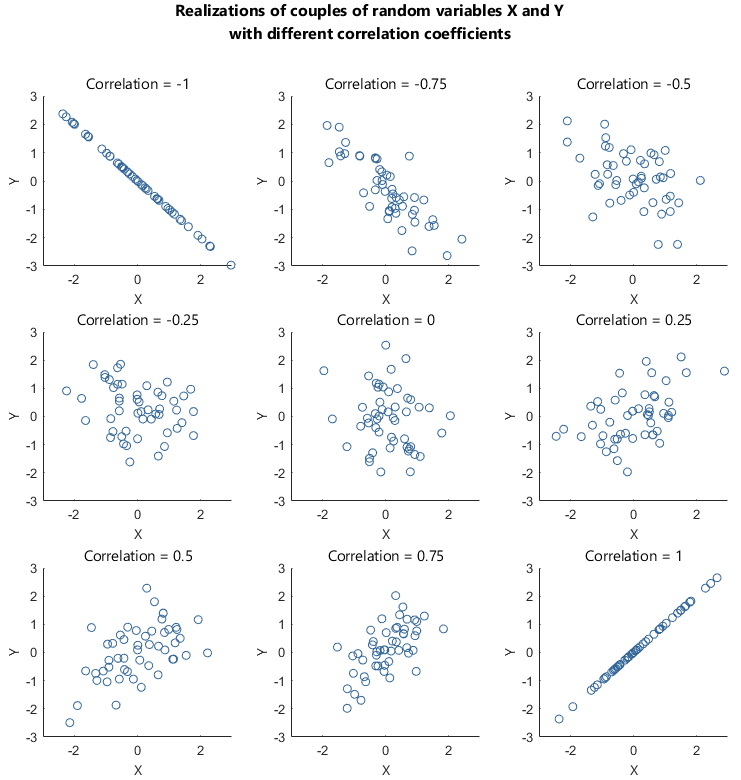

![]() and

and

![]() :

:![]()

Thanks to this property, correlation allows us to easily understand the intensity of the linear dependence between two random variables:

the closer correlation is to

![]() ,

the stronger the positive linear dependence between

,

the stronger the positive linear dependence between

![]() and

and

![]() is;

is;

the closer it is to

![]() ,

the stronger the negative linear dependence between

,

the stronger the negative linear dependence between

![]() and

and

![]() is.

is.

The following terminology is often used:

If

![]() then

then

![]() and

and

![]() are said to be positively linearly correlated (or simply

positively correlated).

are said to be positively linearly correlated (or simply

positively correlated).

If

![]() then

then

![]() and

and

![]() are said to be negatively linearly correlated (or simply

negatively correlated).

are said to be negatively linearly correlated (or simply

negatively correlated).

If

![]() then

then

![]() and

and

![]() are said to be linearly correlated (or simply

correlated).

are said to be linearly correlated (or simply

correlated).

If

![]() then

then

![]() and

and

![]() are said to be uncorrelated. Also note that

are said to be uncorrelated. Also note that

![]()

![]() .

Therefore, two random variables

.

Therefore, two random variables

![]() and

and

![]() are uncorrelated whenever

are uncorrelated whenever

![]() .

.

In this example we show how to compute the coefficient of linear correlation between two discrete random variables.

Let

![]() be a

be a

![]() -dimensional

random vector and denote its entries by

-dimensional

random vector and denote its entries by

![]() and

and

![]() .

.

Let the support of

![]() be

be

![]() and

its joint probability

mass function

be

and

its joint probability

mass function

be

The support of

![]() is

is![]() and

its probability mass

function

is

and

its probability mass

function

is

The expected value of

![]() is

is

The expected value of

![]() is

is

The variance of

![]() is

is

The standard deviation of

![]() is

is

The support of

![]() is:

is:![]() and

its probability mass function

is

and

its probability mass function

is

The expected value of

![]() is

is

The expected value of

![]() is

is

The variance of

![]() is

is

The standard deviation of

![]() is

is

Using the transformation

theorem, we can compute the expected value of

![]() :

:![[eq34]](/images/linear-correlation__80.png)

Hence, the covariance between

![]() and

and

![]() is

is![]() and

the linear correlation coefficient

is

and

the linear correlation coefficient

is![[eq36]](/images/linear-correlation__84.png)

The following sections contain more details about the linear correlation coefficient.

Let

![]() be a random variable,

then

be a random variable,

then![]()

This is proved as

follows:where

we have used the fact

that![]()

The linear correlation coefficient is

symmetric:![]()

This is proved as

follows:where

we have used the fact that covariance is

symmetric:![]()

Below you can find some exercises with explained solutions.

Let

![]() be a

be a

![]() discrete random vector and denote its components by

discrete random vector and denote its components by

![]() and

and

![]() .

.

Let the support of

![]() beand

its joint probability mass function

be

beand

its joint probability mass function

be

Compute the coefficient of linear correlation between

![]() and

and

![]() .

.

The support of

![]() is

is![]() and

its marginal

probability mass function

isThe

expected value of

and

its marginal

probability mass function

isThe

expected value of

![]() isThe

expected value of

isThe

expected value of

![]() isThe

variance of

isThe

variance of

![]() isThe

standard deviation of

isThe

standard deviation of

![]() isThe

support of

isThe

support of

![]() is

is![]() and

its marginal probability mass function

isThe

expected value of

and

its marginal probability mass function

isThe

expected value of

![]() isThe

expected value of

isThe

expected value of

![]() isThe

variance of

isThe

variance of

![]() isThe

standard deviation of

isThe

standard deviation of

![]() isUsing

the transformation theorem, we can compute the expected value of

isUsing

the transformation theorem, we can compute the expected value of

![]() :Hence,

the covariance between

:Hence,

the covariance between

![]() and

and

![]() isand

the coefficient of linear correlation between

isand

the coefficient of linear correlation between

![]() and

and

![]() is

is

Let

![]() be a

be a

![]() discrete random vector and denote its entries by

discrete random vector and denote its entries by

![]() and

and

![]() .

.

Let the support of

![]() beand

its joint probability mass function

be

beand

its joint probability mass function

be

Compute the coefficient of linear correlation between

![]() and

and

![]() .

.

The support of

![]() is

is![]() and

its marginal probability mass function

isThe

mean of

and

its marginal probability mass function

isThe

mean of

![]() isThe

expected value of

isThe

expected value of

![]() isThe

variance of

isThe

variance of

![]() isThe

standard deviation of

isThe

standard deviation of

![]() isThe

support of

isThe

support of

![]() is

is![]() and

its probability mass function

isThe

mean of

and

its probability mass function

isThe

mean of

![]() isThe

expected value of

isThe

expected value of

![]() isThe

variance of

isThe

variance of

![]() isThe

standard deviation of

isThe

standard deviation of

![]() isThe

expected value of the product

isThe

expected value of the product

![]() can

be derived using the transformation

theorem

can

be derived using the transformation

theorem![[eq74]](/images/linear-correlation__163.png) Therefore,

putting pieces together, the covariance between

Therefore,

putting pieces together, the covariance between

![]() and

and

![]() isand

the coefficient of linear correlation between

isand

the coefficient of linear correlation between

![]() and

and

![]() is

is

Let

![]() be a continuous

random vector with support

be a continuous

random vector with support

![]() and

let its joint probability density function

be

and

let its joint probability density function

be![[eq79]](/images/linear-correlation__172.png)

Compute the coefficient of linear correlation between

![]() and

and

![]() .

.

The support of

![]() is

is![]() When

When

![]() ,

the marginal

probability density function of

,

the marginal

probability density function of

![]() is

is

![]() ,

while, when

,

while, when

![]() ,

the marginal probability density function of

,

the marginal probability density function of

![]() can be obtained by integrating

can be obtained by integrating

![]() out of the joint probability density as

follows:Thus,

the marginal probability density function of

out of the joint probability density as

follows:Thus,

the marginal probability density function of

![]() isThe

expected value of

isThe

expected value of

![]() isThe

expected value of

isThe

expected value of

![]() isThe

variance of

isThe

variance of

![]() isThe

standard deviation of

isThe

standard deviation of

![]() isThe

support of

isThe

support of

![]() is

is![]() When

When

![]() ,

the marginal probability density function of

,

the marginal probability density function of

![]() is

is

![]() ,

while, when

,

while, when

![]() ,

the marginal probability density function of

,

the marginal probability density function of

![]() can be obtained by integrating

can be obtained by integrating

![]() out of the joint probability density as

follows:We

do not explicitly compute the integral, but we write the marginal probability

density function of

out of the joint probability density as

follows:We

do not explicitly compute the integral, but we write the marginal probability

density function of

![]() as

follows:The

expected value of

as

follows:The

expected value of

![]() is

is![[eq90]](/images/linear-correlation__206.png) The

expected value of

The

expected value of

![]() is

is![[eq91]](/images/linear-correlation__208.png) The

variance of

The

variance of

![]() isThe

standard deviation of

isThe

standard deviation of

![]() isThe

expected value of the product

isThe

expected value of the product

![]() can be computed by using the transformation

theorem:

can be computed by using the transformation

theorem:![[eq94]](/images/linear-correlation__214.png) Hence,

by the covariance formula, the covariance between

Hence,

by the covariance formula, the covariance between

![]() and

and

![]() isand

the coefficient of linear correlation between

isand

the coefficient of linear correlation between

![]() and

and

![]() is

is

Please cite as:

Taboga, Marco (2021). "Linear correlation", Lectures on probability theory and mathematical statistics. Kindle Direct Publishing. Online appendix. https://www.statlect.com/fundamentals-of-probability/linear-correlation.

Most of the learning materials found on this website are now available in a traditional textbook format.