In a test of hypothesis, a critical value is a number that separates two regions:

the critical region, that is, the set of values of the test statistic that lead to a rejection of the null hypothesis;

the acceptance region, that is, the set of values for which the null is not rejected.

![]()

Table of contents

In what follows we are going to use the following notation:

![]() is the test statistic (e.g., a z-statistic);

is the test statistic (e.g., a z-statistic);

![]() is the critical region;

is the critical region;

![]() is the acceptance region.

is the acceptance region.

Thus, the null hypothesis is rejected

if![]() and

it is not rejected

if

and

it is not rejected

if![]()

Here is a formal definition.

Definition

A critical value is a boundary of the acceptance region

![]() .

.

Let us make an example.

Example

If the acceptance region is the

interval![]() then

the critical region

is

then

the critical region

is![]() The

critical values are the two

boundaries

The

critical values are the two

boundaries![[eq5]](data:image/gif;base64,R0lGODlhAQABAIAAANvf7wAAACH5BAEAAAAALAAAAAABAAEAAAICRAEAOw==) If,

for example, the value of the test statistic is

If,

for example, the value of the test statistic is

![]() ,

then

,

then

![]() belongs to the acceptance region and the null hypothesis is not rejected.

belongs to the acceptance region and the null hypothesis is not rejected.

A test is called one-tailed if there is only one critical

value

![]() .

.

There are two cases:

left-tailed test: the null is rejected only

if![]()

right-tailed test: the null is rejected only if

![]()

The following table summarizes the two cases by using the symbols introduced

above.![[eq8]](/images/critical-value__24.png)

Typically,

![]() is chosen so as to a achieve a desired

size of the test.

is chosen so as to a achieve a desired

size of the test.

Remember that the size is the probability of rejecting the null hypothesis

when it is true. Denote it by

![]() .

.

For a left-tailed test, we

have

In the majority of practical cases, the test statistic is a

continuous random

variable. As a consequence, the probability that it takes any specific

value is equal to zero. In particular,

![]()

Thus, we can

write![[eq11]](/images/critical-value__29.png) where

where

![]() is the cumulative distribution

function (cdf) of the test statistic.

is the cumulative distribution

function (cdf) of the test statistic.

All we need to do in order to determine the critical value is to find a

![]() that solves the

equation

that solves the

equation![]()

We explain below how to solve it.

Things are similar for right-tailed tests. In these tests, we

have

Thus, we need to solve the

equation![]()

For the most common distributions such as the

normal

distribution and the

t

distribution, the

equations![]() and

and![]() have no analytical solution.

have no analytical solution.

The reason is that the inverse of the cdf

![]() is not known in closed form.

is not known in closed form.

So, for example, we cannot compute analytically the solution of the first

equation

as![]()

However, virtually any calculator or statistical software has pre-built functions that allow us to easily solve these equations numerically.

The (old-fashioned) alternative is to look up the critical value in special tables called statistical tables. See this lecture if you want to know more about these alternatives.

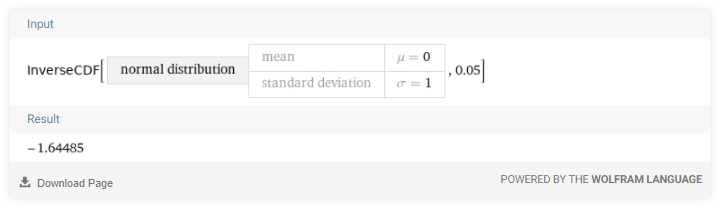

Let us make an example of a left-tailed test.

Suppose that the size of the test is

![]() ,

which means that we are happy with a 5% probability of incorrectly rejecting

the null when it is true.

,

which means that we are happy with a 5% probability of incorrectly rejecting

the null when it is true.

Suppose that our test statistic

![]() has a standard normal distribution.

has a standard normal distribution.

Then, we need to

find![]() where

where

![]() is the cumulative distribution function of a standard normal distribution.

is the cumulative distribution function of a standard normal distribution.

We are going to use a free web app called

Wolfram Alpha to find

![]() .

.

Here is the result.

Thus, the critical value is

![]() .

.

We are going to reject the null hypothesis if

![]() is less than

is less than

![]() .

.

A test is called two-tailed if there are two critical values

![]() and

and

![]() and the null hypothesis is rejected only

if

and the null hypothesis is rejected only

if![]()

We assume without loss of generality that

![]() .

.

Thus, we can add a new line to the table shown in the previous

section:![[eq20]](/images/critical-value__57.png)

As in the case of a one-tailed test (see above), also in the two-tailed case the critical values are chosen so as to achieve a pre-defined size of the test.

The size can be computed as

follows:![[eq21]](/images/critical-value__58.png)

By making again the assumption that the test statistic is a continuous random

variable, we

obtain![]() where

where

![]() is the distribution function of

is the distribution function of

![]() .

.

Our problem is to solve one equation in two unknowns

(![]() and

and

![]() ).

).

There are potentially infinite solutions to the problem because one can choose one of the two critical values at will and choose the remaining one so as to solve the equation.

There is no general rule for choosing one specific solution.

Some possibilities are to:

try and find the solution which maximizes the power of the test in correspondence of a given alternative hypothesis;

find the solution which maximizes the length of the acceptance interval

![]() .

.

We do not discuss these possibilities here, but we refer the reader to Berger and Casella (2002).

We instead discuss the case in which the test statistic has a symmetric

distribution. This is the most relevant case in practice because in many tests

![]() has a normal or a Student's t distribution and both of these distributions are

symmetric.

has a normal or a Student's t distribution and both of these distributions are

symmetric.

A distribution is symmetric (around zero)

when![]() for

any number

for

any number

![]() .

.

We can exploit this fact by making the additional assumption that the two

critical values are

opposite:![]()

Without loss of generality, we can

assumewith

![]() .

.

It follows that the size of the test can be written

as![[eq27]](/images/critical-value__71.png) and

the equation to solve

becomes

and

the equation to solve

becomes![]()

This is an equation in one unknown

(![]() )

that can be solved using the methods (numeric inversion, tables, etc.)

discussed in the previous section on one-tailed tests.

)

that can be solved using the methods (numeric inversion, tables, etc.)

discussed in the previous section on one-tailed tests.

Everything we have said thus far is summarized by the following

table.![[eq29]](/images/critical-value__98.png)

If you want to read a more detailed exposition of the concept of critical value and of related concepts, go to the lecture entitled Hypothesis testing.

Berger, R. L. and G. Casella (2002) "Statistical inference", Duxbury Advanced Series.

Previous entry: Covariance stationary

Next entry: Cross-covariance matrix

Please cite as:

Taboga, Marco (2021). "Critical value", Lectures on probability theory and mathematical statistics. Kindle Direct Publishing. Online appendix. https://www.statlect.com/glossary/critical-value.

Most of the learning materials found on this website are now available in a traditional textbook format.