A sequence of random variables is covariance stationary if:

all the terms of the sequence have the same mean;

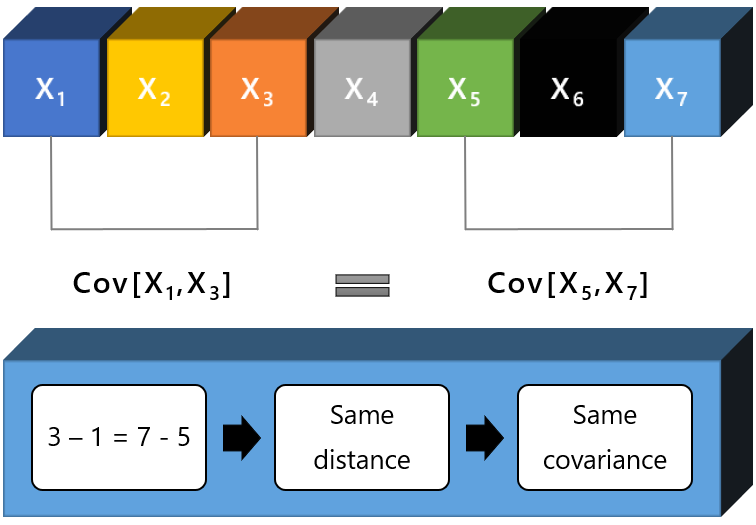

the covariance between any two terms of the sequence depends only on the relative position of the two terms and not on their absolute position.

By relative position of two terms we mean how far apart they are located from each other in the sequence.

Instead, the absolute position refers to where they are located in the sequence.

![]()

Covariance stationary sequences are also called:

weakly stationary sequences;

covariance stationary processes;

weakly stationary processes.

Often, we also use the term time series instead of sequence or process.

This is a formal definition.

Definition

A sequence of random variables

![]() is covariance stationary if and only

if

is covariance stationary if and only

if![[eq2]](/images/covariance-stationary__2.png)

In words:

all the terms of the sequence have mean

![]() ;

;

the covariance

![]() depends only on the relative position

depends only on the relative position

![]() and not on the absolute position

and not on the absolute position

![]() .

.

Note

that![]() which

implies that a weakly stationary process has constant

variance.

which

implies that a weakly stationary process has constant

variance.

The definition above applies without modifications to sequences of random vectors.

In the case of a sequence of vectors,

![]() is a vector of expected values and

is a vector of expected values and

![]() is a matrix of covariances between the entries of the two vectors

is a matrix of covariances between the entries of the two vectors

![]() and

and

![]() (a cross-covariance matrix).

(a cross-covariance matrix).

Let us make some examples.

The simplest example is the so called white noise process, a sequence

![]() that satisfies the following three conditions for any

that satisfies the following three conditions for any

![]() and

and

![]() :

:![[eq8]](data:image/gif;base64,R0lGODlhAQABAIAAANvf7wAAACH5BAEAAAAALAAAAAABAAEAAAICRAEAOw==) where

where

![]() is a positive constant.

is a positive constant.

Let

![]() be the white noise process of the previous example.

be the white noise process of the previous example.

A first-order autoregressive process is a sequence

![]() whose terms

satisfy

whose terms

satisfy![]() where

where

![]() is a constant and the recursion starts from a random variable

is a constant and the recursion starts from a random variable

![]() uncorrelated

with the terms of

uncorrelated

with the terms of

![]() .

.

The expected values

of the terms of the sequence

are![[eq13]](/images/covariance-stationary__23.png)

For the process

![]() to be weakly stationary, the first condition that needs to be satisfied is

to be weakly stationary, the first condition that needs to be satisfied is

![]() which

is satisfied only if

which

is satisfied only if

![]() or

or

![]() .

The latter possibility wil be ruled out below.

.

The latter possibility wil be ruled out below.

The variances

are![[eq18]](/images/covariance-stationary__28.png)

The variances remain finite as

![]() grows only if

grows only if

![]() .

Furthermore, the

condition

.

Furthermore, the

condition![]() is

satisfied only

ifwhich

can be shown, for example, by

solving

is

satisfied only

ifwhich

can be shown, for example, by

solving![[eq21]](/images/covariance-stationary__33.png)

As proved in the lecture on

autocorrelation,

the covariance between any two terms of the sequence

is![]() which

satisfies the condition stated in the definition of weak stationarity (the

covariance depends only on

which

satisfies the condition stated in the definition of weak stationarity (the

covariance depends only on

![]() ).

).

Thus, the sequence

![]() is covariance stationary only

if

is covariance stationary only

if

A stronger concept of stationarity is that of strict stationarity.

A sequence

![]() is said to be strictly stationary if and only if

is said to be strictly stationary if and only if

![]() and

and

![]() have

the same joint distribution for

any

have

the same joint distribution for

any

![]() ,

,

![]() and

and

![]() .

.

The concept of covariance stationarity is often used in probability, statistics and time-series analysis.

Here are some examples:

it is used to compute the autocorrelation function of a process;

it is used to derive Laws of Large Numbers for correlated sequences.

Other concepts related to covariance stationarity can be found in the lecture on sequences of random variables.

Previous entry: Covariance formula

Next entry: Critical value

Please cite as:

Taboga, Marco (2021). "Covariance stationary", Lectures on probability theory and mathematical statistics. Kindle Direct Publishing. Online appendix. https://www.statlect.com/glossary/covariance-stationary.

Most of the learning materials found on this website are now available in a traditional textbook format.