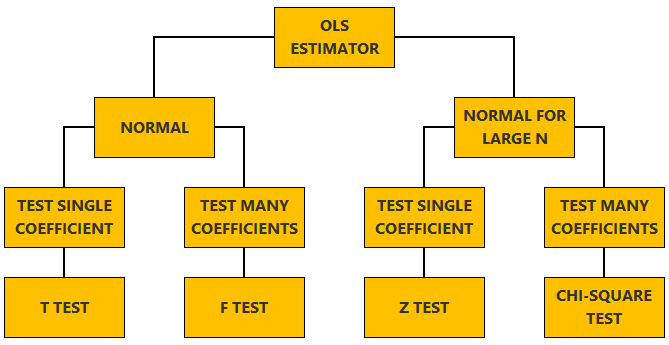

This lecture discusses how to perform tests of hypotheses about the coefficients of a linear regression model estimated by ordinary least squares (OLS).

![]()

Table of contents

The lecture is divided in two parts:

in the first part, we discuss hypothesis testing in the normal linear regression model, in which the OLS estimator of the coefficients has a normal distribution conditional on the matrix of regressors;

in the second part, we show how to carry out hypothesis tests in linear regression analyses where the hypothesis of normality holds only in large samples (i.e., the OLS estimator can be proved to be asymptotically normal).

The regression model

is![[eq1]](data:image/gif;base64,R0lGODlhAQABAIAAANvf7wAAACH5BAEAAAAALAAAAAABAAEAAAICRAEAOw==) where:

where:

![]() is an output variable;

is an output variable;

![]() is a

is a

![]() vector of inputs;

vector of inputs;

![]() is a

is a

![]() vector of coefficients;

vector of coefficients;

![]() is an error term.

is an error term.

There are

![]() observations in the sample, so that

observations in the sample, so that

![]() .

.

We also denote:

by

![]() the

the

![]() vector of

outputs

vector of

outputs

by

![]() the

the

![]() matrix of

inputs

matrix of

inputs

by

![]() the

the

![]() vector of errors

vector of errors

Using this notation, we can

write![]()

Moreover, the OLS estimator of

![]() is

is

![]()

We assume that the design matrix

![]() has full-rank, so that the

matrix

has full-rank, so that the

matrix

![]() is invertible.

is invertible.

We now explain how to derive tests about the coefficients of the normal linear regression model.

The vector of errors

![]() is assumed to have a multivariate normal

distribution conditional on

is assumed to have a multivariate normal

distribution conditional on

![]() ,

with mean equal to

,

with mean equal to

![]() and covariance matrix equal

to

and covariance matrix equal

to![]() where

where

![]() is the

is the

![]() identity matrix and

identity matrix and

![]() is a positive constant.

is a positive constant.

It can be proved (see the lecture about the normal linear regression model) that the assumption of conditional normality implies that:

the OLS estimator

![]() is conditionally multivariate normal with mean

is conditionally multivariate normal with mean

![]() and covariance

matrix

and covariance

matrix

![]() ;

;

the adjusted sample variance of the

residualsis

an unbiased estimator of

![]() ;

furthermore, it has a

Gamma

distribution with parameters

;

furthermore, it has a

Gamma

distribution with parameters

![]() and

and

![]() ;

;

![]() is conditionally independent of

is conditionally independent of

![]() .

.

In a test of a restriction on a single coefficient, we test the

null

hypothesis![]() where

where

![]() is the

is the

![]() -th

entry of the vector of coefficients

-th

entry of the vector of coefficients

![]() and

and

![]() .

.

In other words, our null hypothesis is that the

![]() -th

coefficient is equal to a specific value.

-th

coefficient is equal to a specific value.

This hypothesis is tested with the test

statisticwhere

![]() is the

is the

![]() -th

diagonal entry of the matrix

-th

diagonal entry of the matrix

![]() .

.

The test statistic

![]() has a standard

Student's t distribution with

has a standard

Student's t distribution with

![]() degrees of freedom. For this reason, it is called a t

statistic and the test is called a t test.

degrees of freedom. For this reason, it is called a t

statistic and the test is called a t test.

Under the null hypothesis

![]() has a normal distribution with mean

has a normal distribution with mean

![]() and variance

and variance

![]() .

As a consequence, the

ratiohas

a standard normal distribution (mean

.

As a consequence, the

ratiohas

a standard normal distribution (mean

![]() and variance

and variance

![]() ).

We can

writeSince

).

We can

writeSince

![]() has a Gamma

distribution with parameters

has a Gamma

distribution with parameters

![]() and

and

![]() ,

the

ratiohas

a Gamma distribution with parameters

,

the

ratiohas

a Gamma distribution with parameters

![]() and

and

![]() .

It is also independent of

.

It is also independent of

![]() because

because

![]() is independent of

is independent of

![]() .

Therefore, the

ratiohas

a standard Student's t distribution with

.

Therefore, the

ratiohas

a standard Student's t distribution with

![]() degrees of freedom (see the lecture on the

Student's t

distribution).

degrees of freedom (see the lecture on the

Student's t

distribution).

The null hypothesis is rejected if

![]() falls outside the acceptance region.

falls outside the acceptance region.

How the acceptance region is determined depends not only on the desired size of the test, but also on whether the test is:

two-tailed

(![]() could be smaller or larger than

could be smaller or larger than

![]() ;

we do not exclude either of the two possibilities)

;

we do not exclude either of the two possibilities)

one-tailed (only one of the two things, i.e., either smaller or larger, is possible).

For more details on how to determine the acceptance region, see the glossary entry on critical values.

When testing a set of linear restrictions, we test the null

hypothesis![]() where

where

![]() is a

is a

![]() matrix and

matrix and

![]() is a

is a

![]() vector.

vector.

![]() is the number of restrictions.

is the number of restrictions.

Example

Suppose that

![]() is

is

![]() and that we want to test the hypothesis

and that we want to test the hypothesis

![]() .

We can write it in the form

.

We can write it in the form

![]() by

setting

by

setting

Example

Suppose that

![]() is

is

![]() and that we want to test whether the two restrictions

and that we want to test whether the two restrictions

![]() and

and

![]() hold simultaneously. The first restriction can be written

as

hold simultaneously. The first restriction can be written

as![]() So

we

have

So

we

have

To test the null hypothesis, we use the test

statistic![[eq28]](/images/linear-regression-hypothesis-testing__90.png) which

has an F distribution

with

which

has an F distribution

with

![]() and

and

![]() degrees of freedom. For this reason, it is called an F

statistic and the test is called an F test.

degrees of freedom. For this reason, it is called an F

statistic and the test is called an F test.

Under the null and conditional on

![]() ,

the vector

,

the vector

![]() ,

being a

linear

transformation of the normal random vector

,

being a

linear

transformation of the normal random vector

![]() ,

has a multivariate normal distribution with

mean

,

has a multivariate normal distribution with

mean![[eq29]](/images/linear-regression-hypothesis-testing__96.png) and

covariance

matrixThus,

we can

write

and

covariance

matrixThus,

we can

write![[eq31]](/images/linear-regression-hypothesis-testing__98.png) Since

Since

![]() is multivariate normal, the quadratic form

is multivariate normal, the quadratic form

![]() has a Chi-square distribution with

has a Chi-square distribution with

![]() degrees of freedom (see the lecture on

quadratic

forms involving normal vectors). Furthermore, since

degrees of freedom (see the lecture on

quadratic

forms involving normal vectors). Furthermore, since

![]() has a Gamma distribution with parameters

has a Gamma distribution with parameters

![]() and

and

![]() the

statistichas

a Chi-square distribution with

the

statistichas

a Chi-square distribution with

![]() degrees of freedom (see the lecture on the

Gamma

distribution). Thus, we can

write

degrees of freedom (see the lecture on the

Gamma

distribution). Thus, we can

write![[eq34]](/images/linear-regression-hypothesis-testing__107.png) Thus

Thus

![]() is a ratio between two Chi-square variables, each divided by its degrees of

freedom. The two variables are independent because

is a ratio between two Chi-square variables, each divided by its degrees of

freedom. The two variables are independent because

![]() depends only on

depends only on

![]() and

and

![]() depends only on

depends only on

![]() ,

and

,

and

![]() and

and

![]() are independent. As a consequence,

are independent. As a consequence,

![]() has an F distribution with

has an F distribution with

![]() and

and

![]() degrees of freedom (see the lecture on the

F distribution).

degrees of freedom (see the lecture on the

F distribution).

The F test is one-tailed.

A critical value in the right tail of the F distribution is chosen so as to achieve the desired size of the test.

Then, the null hypothesis is rejected if the F statistics is larger than the critical value.

When you use a statistical package to run a linear regression, you often get a

regression output that includes the value of an F statistic. Usually this is

obtained by performing an F test of the null hypothesis that all the

regression coefficients are equal to

![]() (except the coefficient on the intercept).

(except the coefficient on the intercept).

As we explained in the lecture on

maximum

likelihood estimation of regression models, the maximum likelihood

estimator of the vector of coefficients of a normal linear regression model is

equal to the OLS estimator

![]() .

.

As a consequence, all the usual

tests

based on maximum likelihood procedures (e.g.,

Wald,

Lagrange multiplier,

likelihood

ratio) can be employed to conduct tests of hypothesis about

![]() .

.

In this section we explain how to perform hypothesis tests about the coefficients of a linear regression model when the OLS estimator is asymptotically normal.

As we have shown in the lecture on the properties of the OLS estimator, in several cases (i.e., under different sets of assumptions) it can be proved that:

the OLS estimator

![]() is asymptotically normal, that

is,

is asymptotically normal, that

is,![]() where

where

![]() denotes convergence

in distribution (as the sample size

denotes convergence

in distribution (as the sample size

![]() tends to infinity), and

tends to infinity), and

![]() is a multivariate normal random vector with mean

is a multivariate normal random vector with mean

![]() and covariance matrix

and covariance matrix

![]() ;

the value of the

;

the value of the

![]() matrix

matrix

![]() depends on the set of assumptions made about the regression model;

depends on the set of assumptions made about the regression model;

it is possible to derive a consistent estimator

![]() of

of

![]() ,

that

is,

,

that

is,![]() where

where

![]() denotes convergence

in probability (again as

denotes convergence

in probability (again as

![]() tends to infinity). The estimator

tends to infinity). The estimator

![]() is an easily computable function of the observed inputs

is an easily computable function of the observed inputs

![]() and

outputs

and

outputs

![]() .

.

These two properties are used to derive the asymptotic distribution of the test statistics used in hypothesis testing.

In a z test the null hypothesis is a restriction on a single

coefficient:![]() where

where

![]() is the

is the

![]() -th

entry of the vector of coefficients

-th

entry of the vector of coefficients

![]() and

and

![]() .

.

The test statistic

iswhere

![]() is the

is the

![]() -th

diagonal entry of the estimator

-th

diagonal entry of the estimator

![]() of the asymptotic covariance matrix.

of the asymptotic covariance matrix.

The test statistic

![]() converges in distribution to a

standard normal

distribution as the sample size

converges in distribution to a

standard normal

distribution as the sample size

![]() increases. For this reason, it is called a z statistic

(because the letter z is often used to denote a standard normal distribution)

and the test is called a z test.

increases. For this reason, it is called a z statistic

(because the letter z is often used to denote a standard normal distribution)

and the test is called a z test.

We can write the z statistic

asBy

assumption, the numerator

![]() converges in distribution to a normal random variable

converges in distribution to a normal random variable

![]() with mean

with mean

![]() and variance

and variance

![]() .

The estimated variance

.

The estimated variance

![]() converges in probability to

converges in probability to

![]() ,

so that, by the

Continuous Mapping

theorem, the denominator

,

so that, by the

Continuous Mapping

theorem, the denominator

![]() converges in probability to

converges in probability to

![]() .

Thus, by Slutsky's theorem,

we have that

.

Thus, by Slutsky's theorem,

we have that

![]() converges in distribution to the random

variablewhich

is normal with

meanand

varianceTherefore,

the test statistic

converges in distribution to the random

variablewhich

is normal with

meanand

varianceTherefore,

the test statistic

![]() converges in distribution to

converges in distribution to

![]() ,

which is a standard normal random variable.

,

which is a standard normal random variable.

When

![]() is large, we approximate the actual distribution of

is large, we approximate the actual distribution of

![]() with its asymptotic one (standard normal).

with its asymptotic one (standard normal).

We then employ the test statistic

![]() in the usual manner: based on the desired size of the test and on the

distribution of

in the usual manner: based on the desired size of the test and on the

distribution of

![]() ,

we determine the critical value(s) and the acceptance region.

,

we determine the critical value(s) and the acceptance region.

The test can be either one-tailed or two-tailed. The same comments made for the t-test apply here.

The null hypothesis is rejected if

![]() falls outside the acceptance region.

falls outside the acceptance region.

In a Chi-square test, the null hypothesis is a set of

![]() linear

restrictions

linear

restrictions![]() where

where

![]() is a

is a

![]() matrix and

matrix and

![]() is a

is a

![]() vector.

vector.

The test statistic

is![[eq50]](/images/linear-regression-hypothesis-testing__175.png) which

converges to a

Chi-square

distribution with

which

converges to a

Chi-square

distribution with

![]() degrees of freedom. For this reason, it is called a Chi-square

statistic and the test is called a Chi-square test.

degrees of freedom. For this reason, it is called a Chi-square

statistic and the test is called a Chi-square test.

We can write the test statistic

as![[eq51]](/images/linear-regression-hypothesis-testing__177.png) By

the assumptions on the convergence of

By

the assumptions on the convergence of

![]() and

and

![]() ,

and by the Continuous Mapping theorem, we have

thatBy

Slutsky's theorem, we

have

,

and by the Continuous Mapping theorem, we have

thatBy

Slutsky's theorem, we

have![]() But

But

![]() is multivariate normal with

mean

is multivariate normal with

mean![]() and

variance

and

variance![]() Thus,

Thus,![]() but,

by

standard

results on normal quadratic forms, the quadratic form on the right hand

side has a Chi-square distribution with

but,

by

standard

results on normal quadratic forms, the quadratic form on the right hand

side has a Chi-square distribution with

![]() degrees of freedom

(

degrees of freedom

(![]() is the dimension of the vector

is the dimension of the vector

![]() )

)

When setting up the test, the actual distribution of

![]() is approximated by the asymptotic one (Chi-square).

is approximated by the asymptotic one (Chi-square).

Like the F test, also the Chi-square test is usually one-tailed.

The desired size of the test is achieved by appropriately choosing a critical value in the right tail of the Chi-square distribution.

The null is rejected if the Chi-square statistics is larger than the critical value.

Want to learn more about regression analysis? Here are some suggestions:

Please cite as:

Taboga, Marco (2021). "Linear regression - Hypothesis testing", Lectures on probability theory and mathematical statistics. Kindle Direct Publishing. Online appendix. https://www.statlect.com/fundamentals-of-statistics/linear-regression-hypothesis-testing.

Most of the learning materials found on this website are now available in a traditional textbook format.